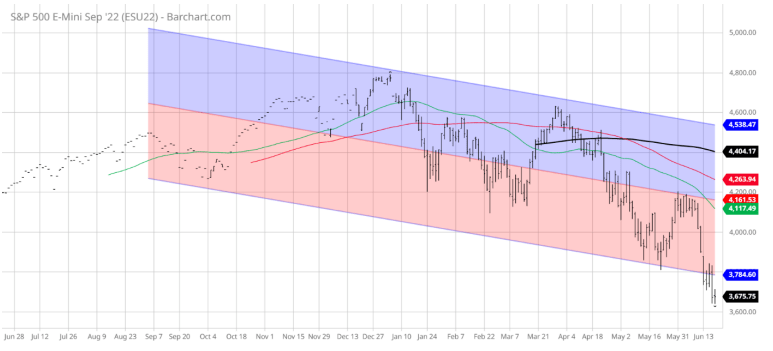

Last week S&P500 officially entered the bear market with the total drawdown of 23.41% YTD. The 4% selloff for the week was triggered by the sharp increase in real interest rates (reaction to the official beginning of the QT) and the new peak in the Fed hawkishness (or expectations of monetary policy tightening). This is still the Phase 1 selloff or the Liquidity Shock, which is likely to continue until we get some positive inflation data – and more clarity in the Fed’s monetary policy tightening.

On positive side, the BE inflation expectations decreased last week. The probability of an imminent recession is still low (based in the 2Y-3mo spread), and credit risk is still low/moderate. Technically, the next support for S&P500 is the 3500 level. The liquidity risk remains the key driver.

Here is the full report.