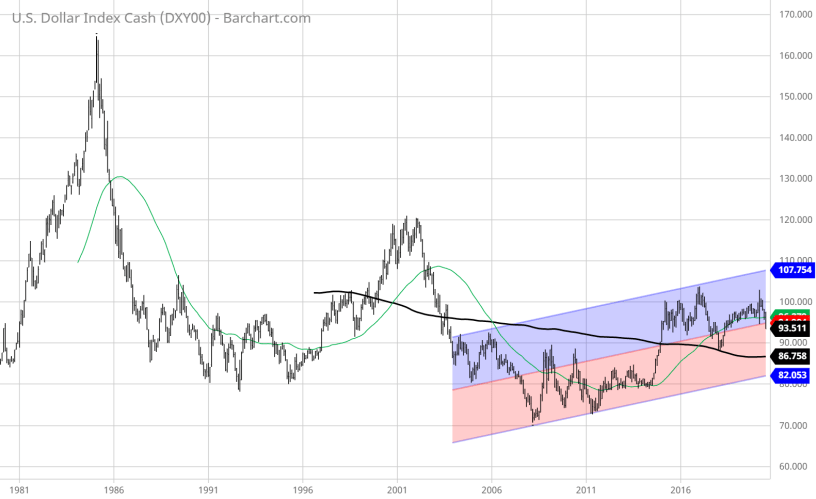

Pre-pandemic trend: Strong USD

One of the key pre-pandemic themes was the strong dollar trade, mainly due to the underlying de-globalization trend. Specifically, the US-China trade war was slowing down the Chinese economy, as well as the export-dependent EU economies, and commodity related EM economics, while the US economy was not as affected.

Early Pandemic Trend: Strong USD

As the pandemic struck, the strong dollar trade accelerated, mostly due to the global dollar shortage, widespread margin calls and the expected EM debt defaults. Stocks and commodities, including gold, dropped, as well as most currencies vs the USD.

Since March 23rd: The Liquidity Driven Weak USD Trend

To save the day, the Fed implemented swap-lines with various global central banks to ease the dollar shortage, which essentially initiated the weak-dollar trade. The sell-everything trade (stocks, commodities, gold, bonds, etc) and buy USD turned into the liquidity-driven buy-everything trade and sell USD. Since March 23rd bottom until now, the weak dollar trade continues . For how long?

USD Bulls argue that: the US economic recovery is stalling due to the failed response to the covid-crisis, while the recovery in the EU and China is picking up, and the undisputed reserve currency status of the US Dollar is at least shaken up due to the geopolitical situation, the US pre-election social unrests, and excessive monetary and fiscal stimulus.

De-globalization = Strong Dollar?

Everybody seems to forget that the unfolding de-globalization will continue to hurt the Chinese economy (and thus the global economy) much more than the US economy. The longer-term USD trend is more likely to reflect the unfolding de-globalization theme. The key variable will be the USD reserve currency status – which at this point is premature to rule out.

Over the short term, the liquidity-driven weak-dollar trade is likely to continue due to widespread speculation, but this is not a weak-USD environment, like the globalization fueled period of 2002-2007.