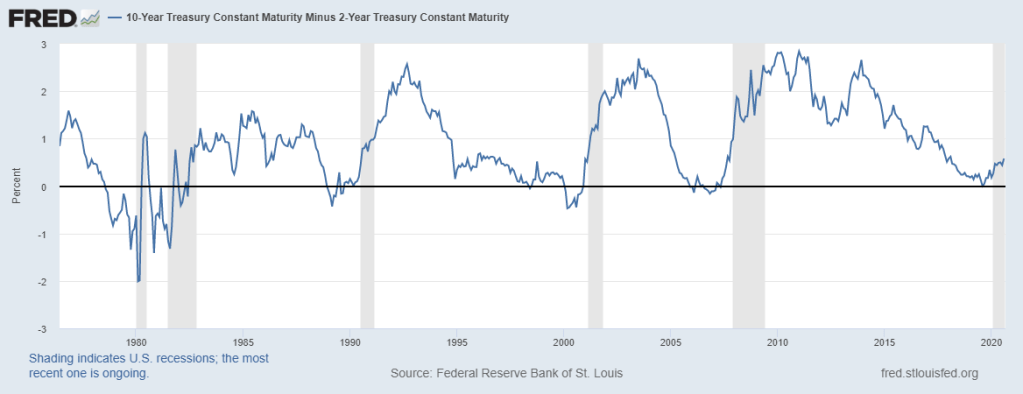

Here are the facts: 1) the US economy is in a recession, 2) the Yield curve is near flat, and 3) the nominal interest rates are near the zero percent level. Historically, at the onset of a recession, the Fed lowers the short term interest rates and steepens the yield curve, which eventually restarts the new growth cycle (see the figure below).

The Desperate Moment

Unlike the previous recessionary cycles, the yield curve is currently near flat, and it must steepen for recovery to take place. How? The nominal rates are near 0%. There are two options.

- Use the European model and lower the short term interest rates below 0%.- the negative interest rates policy, or

- Try to engineer higher long term interest rates, while holding short term interest rates near 0% for longer.

Clearly, the Fed is currently trying to boost the longer term inflation expectations to cause higher longer term interest rates and steepen the yield curve – option 2. Specifically, the Fed’s revised policy calls for targeting a symmetric 2% inflation target, which allows for higher inflation (above 2%) in some periods. In order for this strategy to work, the yield on 10Y Treasury Bond must rise above 2% to steepen the yield curve to a level comparable to the previous recessionary episodes.

In other words, the Fed is trying to talk up inflation – true desperation. But it could work in combination with 1) an extraordinary fiscal stimulus, and 2) de-globalization and trade barriers.